Whatever you enjoy now,

keep it going later

Life is more than paying bills and showing up for work - it’s the little things, and sometimes not-so-little things, that make life feel special. Later in life, this is no different. A daily latte, weekends away, your gym membership - these might be part of your normal everyday routine and easily affordable while you’re working, but once you stop, you’ll still want to enjoy these moments. That’s where retirement planning becomes essential.

Be smart, be secure – be future ready

Recent insights

Insurance Europe Pan-European Pension Survey

This survey shows just how important pension planning is for people in Ireland:

-

![]()

35-40%

of Irish respondents say they are not familiar with how the Irish pension system works

-

![]()

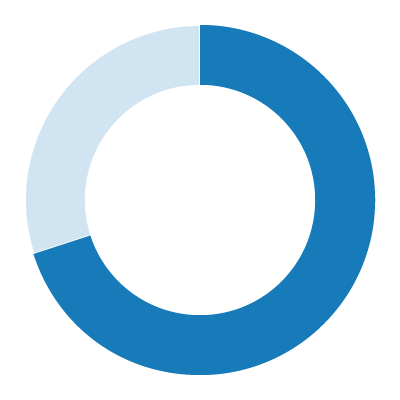

70%

believe they’ll need additional private savings to maintain their standard of living after retirement

-

![]()

45-50%

Many expect that the State and workplace pensions together will only provide around 45–50% of their final salary

So, take a moment to consider your own situation. What do you want your retirement to look like, and how much might you need to fund it?

Knowing this early, and taking action as soon as possible, can make a real difference and most importantly it can help you to ‘Mind the Gap’ - the difference between what you may need in the future and what you’re currently on track to have, giving you the clarity to plan with confidence.

Everyone’s needs are different, so it’s important to invest in a pension plan that meets your future lifestyle and income needs.

What is the pension “gap”?

The pension gap is the difference between what you’re likely to have in retirement and what you may actually need to maintain your lifestyle. Many people assume the State Pension and their work-related pension will be enough, but recent figures show that most Irish people expect these to replace only 45–50% of their final salary.

However, the average person may need around 80% of their current income to maintain a similar standard of living in retirement. That shortfall is the “gap”, and the sooner you understand it, the easier it is to close.

Your pension gap depends on factors like your age, savings to date, future contributions, retirement age, and lifestyle expectations. We want to help you to ‘Mind the Gap’ and be prepared for the future you want to have later in life.

How do I know what retirement savings I will need?

The amount you will need depends on the lifestyle you want later in life, for example everyday spending, hobbies, travel, and the small luxuries you enjoy now. Most people underestimate this.

According to recent figures, 70%+ of Irish people believe they will need additional private savings to maintain their standard of living after they retire. This highlights the importance of understanding your own future needs.

A useful guide is aiming for retirement income that’s around 80% of your working income. A pension adviser can help you project your retirement income, identify any gap, and make a plan to close it.

How much will I receive from the State Pension?

The State Pension provides a foundation for retirement income, but it is not designed to replace a full salary. Most Irish workers will receive the Contributory State Pension, which provides a fixed weekly amount (which is currently €289.30), if you have enough PRSI contributions.

This means the State Pension on its own may fall significantly short of what you need, which is why many people choose to save into a pension to supplement it and close the gap.

How much should I be contributing to my pension?

There’s no one-size-fits-all answer, but a helpful principle is:

the earlier you start, the less you need to contribute each month and the more time your money has to grow.

If you’re starting later, you may need to contribute more to close the gap. Many people increase their pension contributions during higher-earning years or when financial commitments like childcare or mortgages reduce.

Given that 35–40% of Irish people feel unfamiliar with how the pension system works, it can be reassuring to speak with a pension adviser, who can give guidance on what contribution level is appropriate for your age, income and retirement goals.

When should I start saving, and is it too late if I’m older?

The best time to start saving is as early as you can, because long-term growth and compounding can make a significant difference over time. But if you’re starting later in life, it’s not too late as many people don’t focus on their pension until their 40s or 50s.

Increasing contributions, making Additional Voluntary Contributions (AVCs), and reviewing your investment choices can all help strengthen your retirement income.

With many Irish people expecting a shortfall between State/occupational pensions and their needs in retirement, taking action at any stage, preferably as early as possible, can help close your personal pension gap.

Do I have to join auto-enrolment, or should I consider a private pension?

With auto-enrolment having commenced in Ireland, eligible workers who aren’t already in a pension scheme will be automatically enrolled into a retirement savings plan. This makes it easier for people to start saving if they haven’t already.

However, many people prefer the flexibility of a private pension - such as a Personal Pension or PRSA - where they can choose contribution levels, investment options, and manage their pension if they change jobs.

Interestingly, 60–65% of Irish respondents say they would be more likely to invest in a pension product with a European or national certification label, showing that trust and transparency are important when choosing a pension.

A pension adviser can help you compare auto-enrolment with private pensions and decide which option best fits your needs and goals.

Have any more questions?

Speak with a pension advisor today: